Red Hat (RHT) had impressive improvements in revenues and net income (profits) in its fourth quarter (its 3rd fiscal 2011 quarter). For details, see my Red Hat analyst call summary for the December 21st call.

Still, while Red Hat is a great company, its price-to-earnings ratio is much higher than many other good, rapidly growing technology companies. So at this price it is for momentum players and those who can wait a few years to see its profits catch up to the expectations. I don't own any Red Had stock presently, but did when it had a lower P/E ratio.

Red Hat specializes in Linux for the enterprise and related technologies.

Wednesday, December 29, 2010

Tuesday, December 14, 2010

Onyx Pharmaceuticals Clinical Trial Overview

I listened to the Onyx Pharmaceuticals (ONXX) presentation to analysts today. It mainly reported on Onyx's therapeutic pipeline. I have covered Onyx in more depth elsewhere (see my Onyx Pharmaceuticals ONXX page); here I am just recording my immediate impressions from the presentations.

Carfilzomib for multiple myeloma data seems to be excellent. Carfilzomib could become the drug of choice for MM patients. Revenues could begin in late 2011, but would more likely be a 2012 story (they already got a large milestone payment from Ono Pharmaceutical in Japan).

In addition to extending Nexavar (Sorafenib) for liver cancer, there are three main targets for Nexavar: breast, lung, and thyroid cancer.

The breast cancer results seemed somewhat marginal to me. With the right subtype target, they should be able to get results good enough for FDA approval, but it is not a sure thing. A big Phase III trial is about to get underway, which will give everyone a much better view.

The lung cancer results seemed fairly solid, again with the best chance of success being based on subtype identification. I would give Nexavar a better-than-average chance of approval based on data available so far.

The best data appeared to be for thyroid cancer. Here we have a good combination of a lack of any good therapy availability to date and the method of action of Nexavar working out well for the most common type of thyroid cancer. I would bet this indication will be approved.

In the short run, the biggest impact on the stock would come from the approval of reimbursement for Nexavar for liver cancer in South Korea. Liver cancer is far more common in Asia than in the U.S. or Europe (over 10 times as common), so the bulk of the global profits will eventually come from Japan, Korea, and China. China has approved prescribing Nexavar, but not reimbursement for the costs. The Korean approval won't take effect until January 1, so it won't effect Q4 2010 revenues.

My overal impression is that the Onyx stock I own is now very underpriced, but that is based on future trial results, FDA approvals, and marketing successes, so making stock purchases on that assumption involves pretty much risk.

Onyx stock (ONXX) ended the day up $1.04 or 3.1%, at $34.54.

See also Onyx Pharmaceuticals site

Carfilzomib for multiple myeloma data seems to be excellent. Carfilzomib could become the drug of choice for MM patients. Revenues could begin in late 2011, but would more likely be a 2012 story (they already got a large milestone payment from Ono Pharmaceutical in Japan).

In addition to extending Nexavar (Sorafenib) for liver cancer, there are three main targets for Nexavar: breast, lung, and thyroid cancer.

The breast cancer results seemed somewhat marginal to me. With the right subtype target, they should be able to get results good enough for FDA approval, but it is not a sure thing. A big Phase III trial is about to get underway, which will give everyone a much better view.

The lung cancer results seemed fairly solid, again with the best chance of success being based on subtype identification. I would give Nexavar a better-than-average chance of approval based on data available so far.

The best data appeared to be for thyroid cancer. Here we have a good combination of a lack of any good therapy availability to date and the method of action of Nexavar working out well for the most common type of thyroid cancer. I would bet this indication will be approved.

In the short run, the biggest impact on the stock would come from the approval of reimbursement for Nexavar for liver cancer in South Korea. Liver cancer is far more common in Asia than in the U.S. or Europe (over 10 times as common), so the bulk of the global profits will eventually come from Japan, Korea, and China. China has approved prescribing Nexavar, but not reimbursement for the costs. The Korean approval won't take effect until January 1, so it won't effect Q4 2010 revenues.

My overal impression is that the Onyx stock I own is now very underpriced, but that is based on future trial results, FDA approvals, and marketing successes, so making stock purchases on that assumption involves pretty much risk.

Onyx stock (ONXX) ended the day up $1.04 or 3.1%, at $34.54.

See also Onyx Pharmaceuticals site

Saturday, December 11, 2010

Celgene (CELG) ASH Data Points

Revlimid, used to treat MDS (myelodysplastic syndromes) and multiple myeloma, saw revenues increase 44% from Q3 2009. Vidaza, also used to treat MDS, had revenue up 37% y/y. In 2010 Celgene (CELG) stock began at $55.68, yesterday (Friday) it closed at $57.46, so this year has not had a big run up.

That is mainly due to a plunge from some of the data presented at the American Hematological Society (ASH) meeting last weekend. Celgene is trying to show that Revlimid should be used both earlier in the treatment of multiple myeloma and myelodysplastic syndromes (before or coincidental with other therapies) and for a longer duration. Right now "REVLIMID or lenalidomide in combination with dexamethasone is indicated for the treatment of multiple myeloma or MM patients who have received at least one prior therapy." What Celgene wants is Revlimid to be prescribed to new MM patients, without trying any other therapy first.

The data presented in that regard was very positive. See, for instance, Analysis of Revlimid Phase III Study Reports a Significant Improvement in Survival for del(5Q) Myelodysplastic Syndromes and Phase III Study Evaluating Revlimid in Patients with High-Risk Smoldering Multiple Myeloma Reported Statistically Significant Reduction in Risk of Disease Progression. There were many more reports on Celgene products at ASH.

The plunge was due to some data suggesting that patients taking Revlimid for long periods of time had an increased risk for secondary cancers compared to patients taking placebos. This is certainly something to look at; if the increased secondary malignancies are actually caused by Revlimid, rather than a statistical fluctuation (so far the numbers are small), then that would have to be weighted negatively. But Revlimid is not a diet drug, where a few deaths would be weighed against limited benefits. Death is still par for the course with untreated blood cancer patients, and even with treatment. The survival data on patients in the trials has consistently shown that Revlimid prolongs life, and that would include an adverse events, including the development of other cancers.

Mark Shoenebaum, the former Bear Stearns analyst who wrote pointed out the negative data, also pointed out that the results may have been skewed by not looking for secondary tumors in patients whose myeloma progressed, so that Revlimid patients, who had longer times before their myeloma progressed, were not actually compared to a like set of patients.

Celgene stock fell rather dramatically on December 6 (from $60.59 on the prior close to $55.64) as a result of the "news." What this mainly shows is the danger of pricing by auction markets. No one knows if the news is even true, or how significant it is. Buyers disappear, so even normal selling can tank a stock.

Celgene is already trading at a very reasonable forward price to earnings multiple of 22. Most likely Revlimid will be approved for use as a first-line treatment in 2011. In addition, Celgene has an extensive, high-quality pipeline. So my guess is that in a few months the December 6 drop will just look like background noise on the stock charts.

See also:

www.celgene.com

My Celgene Analyst Conference Call summary for Q3 2011

That is mainly due to a plunge from some of the data presented at the American Hematological Society (ASH) meeting last weekend. Celgene is trying to show that Revlimid should be used both earlier in the treatment of multiple myeloma and myelodysplastic syndromes (before or coincidental with other therapies) and for a longer duration. Right now "REVLIMID or lenalidomide in combination with dexamethasone is indicated for the treatment of multiple myeloma or MM patients who have received at least one prior therapy." What Celgene wants is Revlimid to be prescribed to new MM patients, without trying any other therapy first.

The data presented in that regard was very positive. See, for instance, Analysis of Revlimid Phase III Study Reports a Significant Improvement in Survival for del(5Q) Myelodysplastic Syndromes and Phase III Study Evaluating Revlimid in Patients with High-Risk Smoldering Multiple Myeloma Reported Statistically Significant Reduction in Risk of Disease Progression. There were many more reports on Celgene products at ASH.

The plunge was due to some data suggesting that patients taking Revlimid for long periods of time had an increased risk for secondary cancers compared to patients taking placebos. This is certainly something to look at; if the increased secondary malignancies are actually caused by Revlimid, rather than a statistical fluctuation (so far the numbers are small), then that would have to be weighted negatively. But Revlimid is not a diet drug, where a few deaths would be weighed against limited benefits. Death is still par for the course with untreated blood cancer patients, and even with treatment. The survival data on patients in the trials has consistently shown that Revlimid prolongs life, and that would include an adverse events, including the development of other cancers.

Mark Shoenebaum, the former Bear Stearns analyst who wrote pointed out the negative data, also pointed out that the results may have been skewed by not looking for secondary tumors in patients whose myeloma progressed, so that Revlimid patients, who had longer times before their myeloma progressed, were not actually compared to a like set of patients.

Celgene stock fell rather dramatically on December 6 (from $60.59 on the prior close to $55.64) as a result of the "news." What this mainly shows is the danger of pricing by auction markets. No one knows if the news is even true, or how significant it is. Buyers disappear, so even normal selling can tank a stock.

Celgene is already trading at a very reasonable forward price to earnings multiple of 22. Most likely Revlimid will be approved for use as a first-line treatment in 2011. In addition, Celgene has an extensive, high-quality pipeline. So my guess is that in a few months the December 6 drop will just look like background noise on the stock charts.

See also:

www.celgene.com

My Celgene Analyst Conference Call summary for Q3 2011

Tuesday, December 7, 2010

Onyx Pharmaceuticals ASH Carfilzomib Conference Call

Main point is the evidence presented at ASH (American Society of Hematology) that Carfilzomib will be approved eventually by the FDA and become Onyx's (ONXX) second commercial therapy.

Repeated news about working with Ono Pharmaceutical of Japan for Carfilzomib for multiple myeloma. It is in a class of drugs known as proteasome inhibitors. It causes cell death by preventing protein degradation, essentially poisoning the cell with its own products. The hope is that it kills cancer cells with minimal harm to other cell types.

A Phase II trial of Carfilzomib (003a1) has been completed and data was presented at ASH. This was for refractory multiple myeloma, in other words for patients who have received other therapies, but then had the disease progress. Median survival expectation for such patients is currently about 9 months. Study had over 200 patients, endpoint was overall response wait, adjudicated by an independent monitoring committee. Median patient time from diagnosis was 5.4 years. Most patients had pre-existing peripheral neuropathy. Typically had had 5 prior lines of therapy (different drugs). In other words, a very sick, very previously treated group. Overall response rate was 24%, with another 10% with minimal response. Duration of response was 8.3 months, including minimal response patients. Number and type of prior therapies did not seem to influence responses. Median overall survival was 15.5 months. Adverse events were modest for this type of therapy. Conclusion is that Carfilzomib has a robust benefit for this patient population.

004 study of Carfilzomib was a non-randomized 125 patient open label trial also with refractory multiple myeloma, in two dose cohorts. Dexamethasone was administered at beginning of trial. Median age was mid-sixties, about 3.5 years of prior therapy, typically 2 prior lines of therapy, including stem cell transplants in 73 percent. Overall response rate for cohort 1 was 41% cohort 2 was 53%. Responses were relatively fast. Time to progression 8.3 for cohort 1, with cohort 2 median time to progression has not been reached. Typical modest adverse events. Showed a very impressive overall response rate with good tolerance over extended periods of time.

In the trial of therapy naive newly-diagnosed multiple myeloma patients with Carfilzomib plus two current best approved treatments (CRD), with relatively healthy (compared to the two trials above) patients in stage 2 or 3, median age was 59. Neutropenia was surprisingly low and mild, and neuropathy was minimal. 55% complete response rate, one of the best we have seen. 22% had no detectible disease. Nearly 100% had some response. Showed the regimen did not adversely affect stem cell collection. No patient has progressed, and all survived. Concludes regimen is "highly active, demonstrating rapid responses in newly diagnosed myeloma." Consensus of myeloma experts is the results compare favorably to best current therapies.

In refractory patients, many had recieved a different proteosome inhibitor therapy, notably Velcade (Bortezomib). So the response that shows differentiation from other such therapies. In patients who are refractory, the medical community considers minimal response to be significant, but it would not be significant in first-time myeloma patients.

Analysts questioned the characterization of the sickness of patients compared to Velcade trials; the doctors explained why, if anything, the patients were sicker. Patients were able to stay on therapy longer because of the tolerance patients had for it. Doctors insisted "this is the best drug in the myeloma space."

See also:

Onyx Pharmaceuticals site

My Onyx Pharmaceuticals main page

Repeated news about working with Ono Pharmaceutical of Japan for Carfilzomib for multiple myeloma. It is in a class of drugs known as proteasome inhibitors. It causes cell death by preventing protein degradation, essentially poisoning the cell with its own products. The hope is that it kills cancer cells with minimal harm to other cell types.

A Phase II trial of Carfilzomib (003a1) has been completed and data was presented at ASH. This was for refractory multiple myeloma, in other words for patients who have received other therapies, but then had the disease progress. Median survival expectation for such patients is currently about 9 months. Study had over 200 patients, endpoint was overall response wait, adjudicated by an independent monitoring committee. Median patient time from diagnosis was 5.4 years. Most patients had pre-existing peripheral neuropathy. Typically had had 5 prior lines of therapy (different drugs). In other words, a very sick, very previously treated group. Overall response rate was 24%, with another 10% with minimal response. Duration of response was 8.3 months, including minimal response patients. Number and type of prior therapies did not seem to influence responses. Median overall survival was 15.5 months. Adverse events were modest for this type of therapy. Conclusion is that Carfilzomib has a robust benefit for this patient population.

004 study of Carfilzomib was a non-randomized 125 patient open label trial also with refractory multiple myeloma, in two dose cohorts. Dexamethasone was administered at beginning of trial. Median age was mid-sixties, about 3.5 years of prior therapy, typically 2 prior lines of therapy, including stem cell transplants in 73 percent. Overall response rate for cohort 1 was 41% cohort 2 was 53%. Responses were relatively fast. Time to progression 8.3 for cohort 1, with cohort 2 median time to progression has not been reached. Typical modest adverse events. Showed a very impressive overall response rate with good tolerance over extended periods of time.

In the trial of therapy naive newly-diagnosed multiple myeloma patients with Carfilzomib plus two current best approved treatments (CRD), with relatively healthy (compared to the two trials above) patients in stage 2 or 3, median age was 59. Neutropenia was surprisingly low and mild, and neuropathy was minimal. 55% complete response rate, one of the best we have seen. 22% had no detectible disease. Nearly 100% had some response. Showed the regimen did not adversely affect stem cell collection. No patient has progressed, and all survived. Concludes regimen is "highly active, demonstrating rapid responses in newly diagnosed myeloma." Consensus of myeloma experts is the results compare favorably to best current therapies.

In refractory patients, many had recieved a different proteosome inhibitor therapy, notably Velcade (Bortezomib). So the response that shows differentiation from other such therapies. In patients who are refractory, the medical community considers minimal response to be significant, but it would not be significant in first-time myeloma patients.

Analysts questioned the characterization of the sickness of patients compared to Velcade trials; the doctors explained why, if anything, the patients were sicker. Patients were able to stay on therapy longer because of the tolerance patients had for it. Doctors insisted "this is the best drug in the myeloma space."

See also:

Onyx Pharmaceuticals site

My Onyx Pharmaceuticals main page

Tuesday, November 30, 2010

Springtime Economy Cold Spells

Divorced from nature, human minds often make simplistic assumptions about the future. The most common one is that today's trend is tomorrow's trend. That is the kind of thinking that creates financial bubbles.

Think about the season of spring. I know that can be difficult as we enter winter in the northern hemisphere, but it is just a metaphor anyway. So think, perhaps, of last spring. It does not come on all at once, despite being driven by the steady progression of the sun to longer days. There are cycles of cold and warmth.

We may speak of winter returning, but we know as the weeks pass the snow and ice will melt and we will get more frequent warm spells. We even change our definition of warmth. In late winter a warm day may include a night time freeze. In late spring a warm day may miss freezing by 20 degrees.

Development of spring into summer is uneven across geographies. Once state may be having a late winter storm while another has a summer-like day.

So too it is with macroeconomics. We have been through a fairly severe global recession, but it is already summer in China and India. Within the American economy one sector may advance while another remains flat or even declines a bit. In particular in 2010 we saw reduced government spending, but despite that the economy did not collapse. The economy warmed up a fair amount in 2010 despite dire predictions of catastrophe in Europe and a double dip in the U.S. And despite a still-weak housing construction sector.

There are all sorts of signs that the economy is in recovery. That may not be any consolation to those frozen in an unemployed or even homeless status, but it important for investors to see the overall picture accurately. A lot of people panicked and lost a lot of their savings in 2008 when they sold stocks at the bottom of the market. If they had held on, they would be in far better shape now.

Another economic winter will come, to be sure, but we have not even hit late spring yet, much less summer. The way to prepare for winter is to lay aside your winter supplies during the summer, rather than acting as if summer will never end.

2011 should be a good year for the American economy. That does not mean it will be a good year for every single person, or for every business, or every business sector. But hopefully we have, collectively, learned something about the wise use of credit and the need to produce real goods and services in a global economy. Bidding up the prices of things that already exist, be they Beanie Babies or houses, is not a real economic advance.

Stocks can be bid up too high too, but that was not the problem during the latest bubble. Stock prices should reflect the earnings potential of the companies involved. The more profitable companies are, the higher their stock prices should be. The main danger is getting talked into investing in companies that are not profitable, or are obviously going to become unprofitable as the economy changes.

Spring is in the air. Wise investors can hear the birds singing and the wheat and corn sprouting in the fields. If you don't sow, you can't harvest. People who are 100% in bonds should be seriously thinking of rebalancing their portfolios to include stocks again. The value of low interest bonds tends to melt away during the hot days of summer. Better to own CDs at a credit union than bonds once interest rates start rising. And beware the current line of bull about investing in foreign stock funds. Many nations have even less regulation and transparency that the United States. A good rule for investing is don't do it if you don't know what you are doing. There is plenty of risk involved even when you know what you are doing.

See also: Virtuous Economic Cycle Components [September 15, 2010]

Think about the season of spring. I know that can be difficult as we enter winter in the northern hemisphere, but it is just a metaphor anyway. So think, perhaps, of last spring. It does not come on all at once, despite being driven by the steady progression of the sun to longer days. There are cycles of cold and warmth.

We may speak of winter returning, but we know as the weeks pass the snow and ice will melt and we will get more frequent warm spells. We even change our definition of warmth. In late winter a warm day may include a night time freeze. In late spring a warm day may miss freezing by 20 degrees.

Development of spring into summer is uneven across geographies. Once state may be having a late winter storm while another has a summer-like day.

So too it is with macroeconomics. We have been through a fairly severe global recession, but it is already summer in China and India. Within the American economy one sector may advance while another remains flat or even declines a bit. In particular in 2010 we saw reduced government spending, but despite that the economy did not collapse. The economy warmed up a fair amount in 2010 despite dire predictions of catastrophe in Europe and a double dip in the U.S. And despite a still-weak housing construction sector.

There are all sorts of signs that the economy is in recovery. That may not be any consolation to those frozen in an unemployed or even homeless status, but it important for investors to see the overall picture accurately. A lot of people panicked and lost a lot of their savings in 2008 when they sold stocks at the bottom of the market. If they had held on, they would be in far better shape now.

Another economic winter will come, to be sure, but we have not even hit late spring yet, much less summer. The way to prepare for winter is to lay aside your winter supplies during the summer, rather than acting as if summer will never end.

2011 should be a good year for the American economy. That does not mean it will be a good year for every single person, or for every business, or every business sector. But hopefully we have, collectively, learned something about the wise use of credit and the need to produce real goods and services in a global economy. Bidding up the prices of things that already exist, be they Beanie Babies or houses, is not a real economic advance.

Stocks can be bid up too high too, but that was not the problem during the latest bubble. Stock prices should reflect the earnings potential of the companies involved. The more profitable companies are, the higher their stock prices should be. The main danger is getting talked into investing in companies that are not profitable, or are obviously going to become unprofitable as the economy changes.

Spring is in the air. Wise investors can hear the birds singing and the wheat and corn sprouting in the fields. If you don't sow, you can't harvest. People who are 100% in bonds should be seriously thinking of rebalancing their portfolios to include stocks again. The value of low interest bonds tends to melt away during the hot days of summer. Better to own CDs at a credit union than bonds once interest rates start rising. And beware the current line of bull about investing in foreign stock funds. Many nations have even less regulation and transparency that the United States. A good rule for investing is don't do it if you don't know what you are doing. There is plenty of risk involved even when you know what you are doing.

See also: Virtuous Economic Cycle Components [September 15, 2010]

Monday, November 29, 2010

NVIDA Hopes for Tegra processors

Graphics chip maker NVIDIA (NVDA) has had its ups and downs these past few years, and not just because of the recession. Increased competition from AMD in the discrete graphics card market has hurt. So has the accelerating loss of its "chip set" (chips for integrating a cpu to other components) business. At the very high end NVIDIA is getting traction for its Tesla computational chips, but those revenues are not likely to make up for other losses. It is possible NVIDIA will do better in its competition with AMD in 2011, but it is telling financial analysts that Tegra chips for mobile devices are its next big thing.

At its November 11, 2010 analyst conference call and report on its third quarter (Q3, ending October 31, 2010), Tegra was touted as a replacement for lost chip set revenue and more. Note revenue were down 7% y/y to $843.9 million in a period when most semiconductor companies ramped revenues by double digits.

Note also that Tegra has been around for a number of years. What we have been promised in 2010 is a new, improved Tegra, with an improved software stack make the new devices using it something device makers feel can compete with the iPad. This has resulted in a least a half-year delay in releasing product; the products are largely a 2011 story. Management believes that touch-based systems are going to wipe out older systems, and that Tegra will make NVIDIA a serious player in the field.

Maybe, but I am not the only analyst who is a bit skeptical, and with good reason. Tegra 2 might be improved enough to be a revolutionary epicenter in 2011, but it might get lost in the forest of competing platforms. Essentially Tegra combines an ARM CPU with a GeForce GPU, in much the same way that AMD's Fusion chips combine an 8086-based CPU with a Radeon GPU. ARM is a low-power architecture that is being widely used to address the mobile device market.

The problem for NVIDIA is that lots of companies are selling ARM-based processors for mobile devices. Apple designed its own. NVIDIA's advantage would be its graphics technology, but it is not yet clear how much of an advantage they really have. Many companies are using graphics chips, or integrating graphics architecture onto a chip, that was designed, like ARM, to be low-power from the ground up.

The history of Tegra is not one of blazing success. Microsoft Zune and KIN were flops. Maybe the 2011 devices will be better than Apple, but will they sell? They won't be competing with just iPads and iPhones, but with a wide variety of devices. Note too that some of NVIDIA's competitors have huge advantages in the mobile market derived by expertise in areas like Wi-Fi and cell phone modem chips.

For device makers there are a number of competing strategies to choose from. Do you want to start with the best graphics, or perhaps the best cell phone 4G technology? Or if devices become largely indistinguishable, maybe the low price supplier is the key to success.

I have owned NVIDIA stock in the past, but right now I think there are better bargains to be had. If Tegra ramps as rapidly as management would like, then sure, today's stock price looks nice. But I believe this is a wait and see situation. The new Tegra devices may come on the market as early as Q1 2011, but I want to see how they sell through. One popular device could make Tegra viable again, but only Apple seems to be able to guarantee the popularity of its own devices. Once you step outside of Apple, what I mostly see is ruinous competition.

See also:

My NVIDIA analyst call summary for Q3 2010

http://www.nvidia.com/

At its November 11, 2010 analyst conference call and report on its third quarter (Q3, ending October 31, 2010), Tegra was touted as a replacement for lost chip set revenue and more. Note revenue were down 7% y/y to $843.9 million in a period when most semiconductor companies ramped revenues by double digits.

Note also that Tegra has been around for a number of years. What we have been promised in 2010 is a new, improved Tegra, with an improved software stack make the new devices using it something device makers feel can compete with the iPad. This has resulted in a least a half-year delay in releasing product; the products are largely a 2011 story. Management believes that touch-based systems are going to wipe out older systems, and that Tegra will make NVIDIA a serious player in the field.

Maybe, but I am not the only analyst who is a bit skeptical, and with good reason. Tegra 2 might be improved enough to be a revolutionary epicenter in 2011, but it might get lost in the forest of competing platforms. Essentially Tegra combines an ARM CPU with a GeForce GPU, in much the same way that AMD's Fusion chips combine an 8086-based CPU with a Radeon GPU. ARM is a low-power architecture that is being widely used to address the mobile device market.

The problem for NVIDIA is that lots of companies are selling ARM-based processors for mobile devices. Apple designed its own. NVIDIA's advantage would be its graphics technology, but it is not yet clear how much of an advantage they really have. Many companies are using graphics chips, or integrating graphics architecture onto a chip, that was designed, like ARM, to be low-power from the ground up.

The history of Tegra is not one of blazing success. Microsoft Zune and KIN were flops. Maybe the 2011 devices will be better than Apple, but will they sell? They won't be competing with just iPads and iPhones, but with a wide variety of devices. Note too that some of NVIDIA's competitors have huge advantages in the mobile market derived by expertise in areas like Wi-Fi and cell phone modem chips.

For device makers there are a number of competing strategies to choose from. Do you want to start with the best graphics, or perhaps the best cell phone 4G technology? Or if devices become largely indistinguishable, maybe the low price supplier is the key to success.

I have owned NVIDIA stock in the past, but right now I think there are better bargains to be had. If Tegra ramps as rapidly as management would like, then sure, today's stock price looks nice. But I believe this is a wait and see situation. The new Tegra devices may come on the market as early as Q1 2011, but I want to see how they sell through. One popular device could make Tegra viable again, but only Apple seems to be able to guarantee the popularity of its own devices. Once you step outside of Apple, what I mostly see is ruinous competition.

See also:

My NVIDIA analyst call summary for Q3 2010

http://www.nvidia.com/

Sunday, November 28, 2010

Microchip (MCHP) Accelerates Dividends

Microchip continues to be on a roll, with demand for its semiconductor solutions high, and its product sales from its acquisition of SST ramping better than expected. As a result the dividend has been increased again, and the dividend for Q1 2011 has been pulled into December.

There is expected to be a dip in Q4 revenues due to the record shipments of Q3, but sequential growth is expected to resume in Q1 2011.

The GAAP numbers tell the story beautifully, even taking into account revenue increases from the SST acquisition earlier this year. Revenues were $382.3 million, up 19% sequentially from $320.8 million and up 69% from $226.7 million year-earlier. Net income was $103.1 million, up 15% sequentially from $89.6 million and up 132% from $44.5 million year-earlier. EPS (earnings per share) were $0.54, up 13% sequentially from $0.48 and up 125% from $0.24 year-earlier.

As I explained in Microchip Expands Markets, the microcontroller market can be expected to grow for years as microcontrollers are inserted into increasing numbers of appliances (including automobiles) and as the number of appliances expands in nations like China, India, Indonesia, Brazil and developing nations.

Microchip dominates the microcontroller market largely because its multitude of chip variations allow engineers to get the design job done at minimal cost and, if they like, with minimal power consumption. The SST acquisition added a number of key technologies and device types. Microchip sold some SST lines and discontinued others, but announced during its analyst conference call (11/04/2010) that SST Superflash memory and RF lines, which had been listed as discontinued in the prior quarter, had proven to be unexpectedly profitable and now have been un-discontinued.

Orders slowed in September, which would be a negative indicator for Q4 revenues. But after a 20% jump from Q2, I am not worried about a leveling off or slight drop in Q4. I think a lot of equipment makers are being cautious, not sure of consumer sentiment in the U.S. or what's going on with debt issues in Europe. My take is the end demand is actually growing, though we are also seeing more seasonality than last year. With a good consumer season underway in the U.S. and growth still strong in Asia, I don't think Europe will be that much of an issue.

The Q4 dividend of 34.4 cents per share will be payable on December 2, 2010 to stockholders of record back on November 18, 2010. The Q1 dividend of 34.5 cents per share will be paid on December 27, 2010 to shareholders of record on December 13, 2010.

Microchip is a great company for customers, employees, and shareholders, but there are always a variety of risks to consider with any technology company. So ... Keep Diversified!

See also

http://www.microchip.com/

My Microchip analyst call Q3 2010 summary

There is expected to be a dip in Q4 revenues due to the record shipments of Q3, but sequential growth is expected to resume in Q1 2011.

The GAAP numbers tell the story beautifully, even taking into account revenue increases from the SST acquisition earlier this year. Revenues were $382.3 million, up 19% sequentially from $320.8 million and up 69% from $226.7 million year-earlier. Net income was $103.1 million, up 15% sequentially from $89.6 million and up 132% from $44.5 million year-earlier. EPS (earnings per share) were $0.54, up 13% sequentially from $0.48 and up 125% from $0.24 year-earlier.

As I explained in Microchip Expands Markets, the microcontroller market can be expected to grow for years as microcontrollers are inserted into increasing numbers of appliances (including automobiles) and as the number of appliances expands in nations like China, India, Indonesia, Brazil and developing nations.

Microchip dominates the microcontroller market largely because its multitude of chip variations allow engineers to get the design job done at minimal cost and, if they like, with minimal power consumption. The SST acquisition added a number of key technologies and device types. Microchip sold some SST lines and discontinued others, but announced during its analyst conference call (11/04/2010) that SST Superflash memory and RF lines, which had been listed as discontinued in the prior quarter, had proven to be unexpectedly profitable and now have been un-discontinued.

Orders slowed in September, which would be a negative indicator for Q4 revenues. But after a 20% jump from Q2, I am not worried about a leveling off or slight drop in Q4. I think a lot of equipment makers are being cautious, not sure of consumer sentiment in the U.S. or what's going on with debt issues in Europe. My take is the end demand is actually growing, though we are also seeing more seasonality than last year. With a good consumer season underway in the U.S. and growth still strong in Asia, I don't think Europe will be that much of an issue.

The Q4 dividend of 34.4 cents per share will be payable on December 2, 2010 to stockholders of record back on November 18, 2010. The Q1 dividend of 34.5 cents per share will be paid on December 27, 2010 to shareholders of record on December 13, 2010.

Microchip is a great company for customers, employees, and shareholders, but there are always a variety of risks to consider with any technology company. So ... Keep Diversified!

See also

http://www.microchip.com/

My Microchip analyst call Q3 2010 summary

Wednesday, November 24, 2010

SGI Ramps Supercomputer Sales

SGI (Silicon Graphics International) reported calendar third quarter (Q3) results on November 3, 2010. Revenues were $112.9 million, up 12% sequentially from $101.6 million, and up 13% from $100.1 million in the year-earlier quarter. [Actually, these are fiscal Q1 2011 results, for the quarter ending September 24, 2010.]

GAAP net income was negative $11.2 million, up sequentially from negative $27.6 million and up from negative $17.6 million year-earlier. EPS (earnings per share) was negative $0.37, improving sequentially from negative $0.91 and from negative $0.60 year-earlier.

That is modest revenue growth coming off a recession plagued 2009, and well short of hitting a profitable level. Things look better on a non-GAAP basis: Non-GAAP revenue was $130.3 million, up 6% y/y from $122.7 million. Net income negative $1.8 million. Non-GAAP EPS was negative $0.06, improved from negative $0.09 year-earlier. EBIDTA characterized as "positive." But probably not very positive, or they would have given us a number.

Is the new SGI, a combination of Rackable with the old bankrupt SGI, another loser company, unable to keep pace with competitors that can invest more in R&D and can reinvest profits? Maybe not. Maybe management is moving forward at a deliberate pace that really will get the company to break-even in 2011 and profits in 2012. Since the stock price makes the case for the loser scenario (market capitalization end of today was $241 million, about half annual revenues), here I'm going to look at the possible upside.

Q3 was the first full quarter of shipment for Altix UV, SGI's supercomputer offering, and 49 of these systems shipped in the quarter. Silicon Graphics International ships many products besides Altix UV, including racked server systems for datacenters and cloud computing. But I suspect most of the ramp from Q2 to Q3 was from Altix UV.

Service revenue was a healthy 30% of total revenues. Service revenue is usually a steadier stream than hardware revenues when you are selling in chunks as big as SGI does.

Most important of all, SGI reported they entered fiscal Q2 with a strong backlog. There were also large shipments late in the quarter, resulting in a larger accounts receivable than usual, at $96 million.

Altix UV sells mainly to government entities, including research laboratories and universities. But it also can be used for tasks like biotechnology and analysis of oil and gas exploration data. It gives a lot of computing power to these institutions at a very reasonable price. How much demand is out there for 2011, however, is difficult to predict. If the current quarter results come in strong, I would see that as an indicator that calendar 2011 will be a good year.

SGI says that margins on Altix UV are good, partly because of the software stacks that go with the hardware. Margins were a big concern both at the old Rackable and old SGI. I believe that prices on all products should be set to give healthy margins. If competition or lack of demand makes that impossible for particular products, then those product lines should be dropped.

So I'll hold onto my SGI stock and see what the results are for the current quarter. I'd actually like to see more spent on R&D, but only after the company is solidly in the black on a GAAP basis.

See also: Silicon Graphics International web site.

My SGI analyst conference call summaries page

GAAP net income was negative $11.2 million, up sequentially from negative $27.6 million and up from negative $17.6 million year-earlier. EPS (earnings per share) was negative $0.37, improving sequentially from negative $0.91 and from negative $0.60 year-earlier.

That is modest revenue growth coming off a recession plagued 2009, and well short of hitting a profitable level. Things look better on a non-GAAP basis: Non-GAAP revenue was $130.3 million, up 6% y/y from $122.7 million. Net income negative $1.8 million. Non-GAAP EPS was negative $0.06, improved from negative $0.09 year-earlier. EBIDTA characterized as "positive." But probably not very positive, or they would have given us a number.

Is the new SGI, a combination of Rackable with the old bankrupt SGI, another loser company, unable to keep pace with competitors that can invest more in R&D and can reinvest profits? Maybe not. Maybe management is moving forward at a deliberate pace that really will get the company to break-even in 2011 and profits in 2012. Since the stock price makes the case for the loser scenario (market capitalization end of today was $241 million, about half annual revenues), here I'm going to look at the possible upside.

Q3 was the first full quarter of shipment for Altix UV, SGI's supercomputer offering, and 49 of these systems shipped in the quarter. Silicon Graphics International ships many products besides Altix UV, including racked server systems for datacenters and cloud computing. But I suspect most of the ramp from Q2 to Q3 was from Altix UV.

Service revenue was a healthy 30% of total revenues. Service revenue is usually a steadier stream than hardware revenues when you are selling in chunks as big as SGI does.

Most important of all, SGI reported they entered fiscal Q2 with a strong backlog. There were also large shipments late in the quarter, resulting in a larger accounts receivable than usual, at $96 million.

Altix UV sells mainly to government entities, including research laboratories and universities. But it also can be used for tasks like biotechnology and analysis of oil and gas exploration data. It gives a lot of computing power to these institutions at a very reasonable price. How much demand is out there for 2011, however, is difficult to predict. If the current quarter results come in strong, I would see that as an indicator that calendar 2011 will be a good year.

SGI says that margins on Altix UV are good, partly because of the software stacks that go with the hardware. Margins were a big concern both at the old Rackable and old SGI. I believe that prices on all products should be set to give healthy margins. If competition or lack of demand makes that impossible for particular products, then those product lines should be dropped.

So I'll hold onto my SGI stock and see what the results are for the current quarter. I'd actually like to see more spent on R&D, but only after the company is solidly in the black on a GAAP basis.

See also: Silicon Graphics International web site.

My SGI analyst conference call summaries page

Tuesday, November 23, 2010

AMD versus Intel: Show Me the DX 11

New computers in 2011 based on competing processors from Intel and AMD will initiate a new era in personal computing: the combination of a CPU and GPU (graphics processing unit) on a single chip. Intel's offering is refered to as Sandy Bridge; AMD's is Brazos (part of the Fusion program). In both cases a line of processors will be introduced that will be distinguished by part numbers. Systems are being built now and should be first available to consumers in January, with many more systems and variations on the processors available as 2011 progresses.

Over the last decade in particular graphics processing has increased in importance for the vast majority of computer users. People watch and even edit video on a regular basis. 3D virtual realities, including games, are a common part the computer experience. Even business applications are increasingly visual and three dimensiona. Starting with Windows Vista, computers needed improved graphic computation just to allow the operating system to present all of its graphic features.

If there is one thing consumers (including business buyers) need to know about computer graphics, it is that DX 11, introduced with Windows 7 in 2009, is the graphics standard for today's applications. DX 11 is short for DirectX 11, which Microsoft designed to handle multimedia, including video and 3D graphics. The prior generation, DirectX 10, was introduced in 2006. While a powerful advance in that era, it is now seriously out of date. While many applications still use DX 10, most new software introduced in 2011 will run best with DX 11. When DX 11 is not available, they will default to the lower graphics standards of DX 10 or earlier.

When a computer runs a DX 11 game or application by substituting DX 10, it loses graphic details that enhance the visual experience.

Sandy Bridge cannot run DX 11. If you buy a computer with an Intel Sandy Bridge processor, you will have two choices. Sub-optimal graphics, or buying an add-in graphics card from AMD or NVIDIA. AMD's Brazos chips (and all their Fusion chips to be introduced in 2011), on the other hand, do run DX 11. If you think about the computer replacement cycle, this is a remarkable difference. Intel computers bought in 2011 can be expected to remain in use for 2 to 4 years. By the end of that cycle they will be running a decade-old graphics standard.

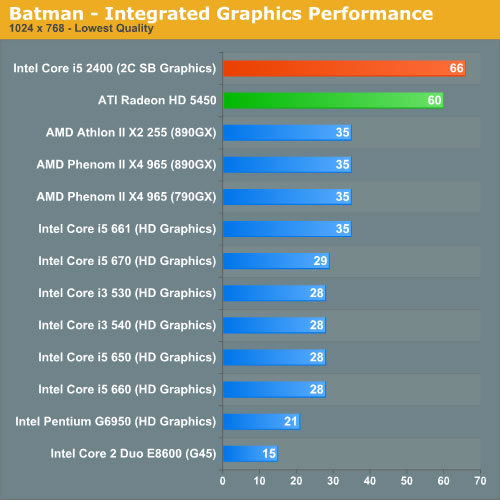

Intel is going to spend a hefty amount of money trying to convince people that Sandy Bridge based computers have graphics on par with AMD Brazos based computers. I've seen some of how that will work already. One online technology reviewer in England used a factually correct article that first appeared at Anandtech to argue that Sandy Bridge is about as good, possibly better, than AMD offerings. He used the following graphic to support his argument [see also the full Sandy Bridge Preview at Anandtech]:

What you see hear is that a desktop Sandy Bridge Core i5 (the top bar) shows a good improvement on Intel's earlier integrated graphics attempts. It is also significantly better, for this particular game, than a AMD Radeon 5450 card. That is great, but it is not a valid comparison for people buying new computers in 2010. The Radeon 5450 card, as you can see from the chart, could do remarkable things for an older Intel CPU with integrated graphics. But it is a card you can now get, retail, for $33.99 [See HD 5450 at TigerDirect]. It supports DX 11. It is the very bottom of the AMD discrete graphics line.

Fair enough, though, Sandy Bridge has the graphics equivalance of the cheapest, slowest discrete video cards made with AMD graphics chips, except it can't do DX 11. Brazos has, as its graphics engine, the equivalent of either a Radeon HD 6250 or 6310, depending on the exact chip used, but those don't correspond to any discrete chips released by AMD. However, graphics capabilities of the Brazos APU are only slightly less than for the 5450.

The Brazos chips, draws just 9 watts of power in the C versions with 6250s, or 18 watts in the E versions with 6310s. The Intel Core i5 2400 draws 95 watts (according to Anandtech). In fact [See Sandy Bridge Preview] they list no Sandy Bridge CPU that draws less than 65 watts.

In other words, in order to make Intel integrated graphics look better than AMD APU graphics, you need to take an expensive, power-sucking chip designed for desktop computers and compare it to a relatively inexpensive, power-sipping chip designed for netbooks and notebooks. And the Intel based desktop computer won't do DX 11.

The way it works out, AMD is releasing its Fusion (combined CPU/GPU) notebook & netbook chips in January. Intel is releasing its desktop chips with integrated graphics January. So direct mobile to mobile and desktop to desktop comparisons are not available yet.

AMD will be releasing more powerful Bulldozer chips designed for desktops later in 2011. They will support DX 11. Intel uses Atom for its netbooks; expect no DX 11 support there.

DX 11 adoption is well underway. Games tend to adopt a new graphics standard most quickly, but only when new games are introduced. See a list of games with DX 11 support. Note that Windows 7 itself supports DX 11. Expect new versions of most major application programs coming out in 2011 and 2012 to support DX 11.

What consumers need to know is that Intel based computers are essentially defective as they come off the assembly lines unless (1) you just do simple tasks like e-mail that are not graphics intensive or (2) they include a discrete graphics card from AMD or NVIDIA.

Who will tell them that? Not Intel. And Intel's advertising budget is such that you can expect a lot of obfuscation in media outlets, including technology magazines and web sites dependent on Intel for much of their advertising revenue. Intel also pays many large retail chains to promote its products over AMD products (by paying for ads).

If anyone is going to get the truth out, it is the millions of ordinary tech people who help everyone else with their buying decisions year-in and year-out. If they can get the typical buyer to ask the typical seller, "Does it do DX 11?" then AMD is going to pick up a lot of market share in 2011. On the other hand, if they stick to the "Intel is the premium brand," line, AMD will continue to have a hard time getting its message heard.

Over the last decade in particular graphics processing has increased in importance for the vast majority of computer users. People watch and even edit video on a regular basis. 3D virtual realities, including games, are a common part the computer experience. Even business applications are increasingly visual and three dimensiona. Starting with Windows Vista, computers needed improved graphic computation just to allow the operating system to present all of its graphic features.

If there is one thing consumers (including business buyers) need to know about computer graphics, it is that DX 11, introduced with Windows 7 in 2009, is the graphics standard for today's applications. DX 11 is short for DirectX 11, which Microsoft designed to handle multimedia, including video and 3D graphics. The prior generation, DirectX 10, was introduced in 2006. While a powerful advance in that era, it is now seriously out of date. While many applications still use DX 10, most new software introduced in 2011 will run best with DX 11. When DX 11 is not available, they will default to the lower graphics standards of DX 10 or earlier.

When a computer runs a DX 11 game or application by substituting DX 10, it loses graphic details that enhance the visual experience.

Sandy Bridge cannot run DX 11. If you buy a computer with an Intel Sandy Bridge processor, you will have two choices. Sub-optimal graphics, or buying an add-in graphics card from AMD or NVIDIA. AMD's Brazos chips (and all their Fusion chips to be introduced in 2011), on the other hand, do run DX 11. If you think about the computer replacement cycle, this is a remarkable difference. Intel computers bought in 2011 can be expected to remain in use for 2 to 4 years. By the end of that cycle they will be running a decade-old graphics standard.

Intel is going to spend a hefty amount of money trying to convince people that Sandy Bridge based computers have graphics on par with AMD Brazos based computers. I've seen some of how that will work already. One online technology reviewer in England used a factually correct article that first appeared at Anandtech to argue that Sandy Bridge is about as good, possibly better, than AMD offerings. He used the following graphic to support his argument [see also the full Sandy Bridge Preview at Anandtech]:

What you see hear is that a desktop Sandy Bridge Core i5 (the top bar) shows a good improvement on Intel's earlier integrated graphics attempts. It is also significantly better, for this particular game, than a AMD Radeon 5450 card. That is great, but it is not a valid comparison for people buying new computers in 2010. The Radeon 5450 card, as you can see from the chart, could do remarkable things for an older Intel CPU with integrated graphics. But it is a card you can now get, retail, for $33.99 [See HD 5450 at TigerDirect]. It supports DX 11. It is the very bottom of the AMD discrete graphics line.

Fair enough, though, Sandy Bridge has the graphics equivalance of the cheapest, slowest discrete video cards made with AMD graphics chips, except it can't do DX 11. Brazos has, as its graphics engine, the equivalent of either a Radeon HD 6250 or 6310, depending on the exact chip used, but those don't correspond to any discrete chips released by AMD. However, graphics capabilities of the Brazos APU are only slightly less than for the 5450.

The Brazos chips, draws just 9 watts of power in the C versions with 6250s, or 18 watts in the E versions with 6310s. The Intel Core i5 2400 draws 95 watts (according to Anandtech). In fact [See Sandy Bridge Preview] they list no Sandy Bridge CPU that draws less than 65 watts.

In other words, in order to make Intel integrated graphics look better than AMD APU graphics, you need to take an expensive, power-sucking chip designed for desktop computers and compare it to a relatively inexpensive, power-sipping chip designed for netbooks and notebooks. And the Intel based desktop computer won't do DX 11.

The way it works out, AMD is releasing its Fusion (combined CPU/GPU) notebook & netbook chips in January. Intel is releasing its desktop chips with integrated graphics January. So direct mobile to mobile and desktop to desktop comparisons are not available yet.

AMD will be releasing more powerful Bulldozer chips designed for desktops later in 2011. They will support DX 11. Intel uses Atom for its netbooks; expect no DX 11 support there.

DX 11 adoption is well underway. Games tend to adopt a new graphics standard most quickly, but only when new games are introduced. See a list of games with DX 11 support. Note that Windows 7 itself supports DX 11. Expect new versions of most major application programs coming out in 2011 and 2012 to support DX 11.

What consumers need to know is that Intel based computers are essentially defective as they come off the assembly lines unless (1) you just do simple tasks like e-mail that are not graphics intensive or (2) they include a discrete graphics card from AMD or NVIDIA.

Who will tell them that? Not Intel. And Intel's advertising budget is such that you can expect a lot of obfuscation in media outlets, including technology magazines and web sites dependent on Intel for much of their advertising revenue. Intel also pays many large retail chains to promote its products over AMD products (by paying for ads).

If anyone is going to get the truth out, it is the millions of ordinary tech people who help everyone else with their buying decisions year-in and year-out. If they can get the typical buyer to ask the typical seller, "Does it do DX 11?" then AMD is going to pick up a lot of market share in 2011. On the other hand, if they stick to the "Intel is the premium brand," line, AMD will continue to have a hard time getting its message heard.

Onyx Pharmaceuticals (ONXX) Jumps on Carfilzomib Revenue

As I have discussed several times, most recently in Onyx Pharmaceuticals Jumps on Carfilzomib Data [August 8, 2010], Onyx Pharmaceuticals (ONXX) could have shown a nice profit in 2009 with revenues from its liver and kidney cancer drug Nexavar. Instead it has spent its potential profits on research and development, seeking proof that Nexavar is effective in more kinds of cancer, and acquiring other potential therapies, notably Carfilzomib.

The payoff from that strategy was seen in the Onyx report on Q3 2010, which included a $59.2 million payment from Ono Pharmaceutical of Japan for the rights to develop and sell Carfilzomib in Japan. Carfilzomib was acquired with Proteolix. Its first indication is for multiple myeloma. It is in a class of drugs known as proteasome inhibitors. It causes cell death by preventing protein degradation, essentially poisoning the cell with its own products. The hope is that it kills cancer cells with minimal harm to other cell types.

A Phase II trial of Carfilzomib has been completed, with full data to be reported at the ASH (American Society of Hematology) meeting beginning December 7th. This trial data may support FDA approval; it has to be very good data to get approval from a phase II trial, because of the small number of patients enrolled. A full Phase III trial is also already being enrolled.

The payment from Ono is not indicative of regular quarterly revenues. Most revenue in 2011 will be from Nexavar sales through Bayer. This means net income may be positive or negative on a quarterly basis. So expect volatility in the stock price. Good news on Carfilzomib will drive the stock higher; there should be a floor under bad news because of Nexavar sales.

Nexavar itself is being tested for further indications: adjuvant liver and kidney cancers; non-small cell lung cancer; thyroid, breast, and ovarian cancer. These trials are mostly in Phase II or early in Phase III.

Onyx currently has 6 additional compounds in preclinical or in clinical trials. In biotechnology it is a good idea to have a wide pipeline, because most promising therapies bomb out at some point. Having six compounds in addition to Nexavar and Carfilzomib is reasonable for a company with Onyx's resources.

Onyx Pharmaceuticals is also sitting on a good pile of cash, $588 million. That is a good cushion for the dicey game of drug development and sales.

On the negative end, while liver cancer sales for Nexavar are still ramping as it gains approval in more countries, kidney cancer sales are about flat, due to increased competition.

I think the chances of Onyx fizzling are reasonably low, and the upside potential is very good. The price ($29.65 as I write) strikes me as still not taking into account its full future profit making potential if Carfilzomib is approved, but it isn't in the bargain basement the way it was earlier this year (52 week low $19.54).

See also:

Onyx Pharmaceuticals site

My Onyx Pharmaceuticals main page

The payoff from that strategy was seen in the Onyx report on Q3 2010, which included a $59.2 million payment from Ono Pharmaceutical of Japan for the rights to develop and sell Carfilzomib in Japan. Carfilzomib was acquired with Proteolix. Its first indication is for multiple myeloma. It is in a class of drugs known as proteasome inhibitors. It causes cell death by preventing protein degradation, essentially poisoning the cell with its own products. The hope is that it kills cancer cells with minimal harm to other cell types.

A Phase II trial of Carfilzomib has been completed, with full data to be reported at the ASH (American Society of Hematology) meeting beginning December 7th. This trial data may support FDA approval; it has to be very good data to get approval from a phase II trial, because of the small number of patients enrolled. A full Phase III trial is also already being enrolled.

The payment from Ono is not indicative of regular quarterly revenues. Most revenue in 2011 will be from Nexavar sales through Bayer. This means net income may be positive or negative on a quarterly basis. So expect volatility in the stock price. Good news on Carfilzomib will drive the stock higher; there should be a floor under bad news because of Nexavar sales.

Nexavar itself is being tested for further indications: adjuvant liver and kidney cancers; non-small cell lung cancer; thyroid, breast, and ovarian cancer. These trials are mostly in Phase II or early in Phase III.

Onyx currently has 6 additional compounds in preclinical or in clinical trials. In biotechnology it is a good idea to have a wide pipeline, because most promising therapies bomb out at some point. Having six compounds in addition to Nexavar and Carfilzomib is reasonable for a company with Onyx's resources.

Onyx Pharmaceuticals is also sitting on a good pile of cash, $588 million. That is a good cushion for the dicey game of drug development and sales.

On the negative end, while liver cancer sales for Nexavar are still ramping as it gains approval in more countries, kidney cancer sales are about flat, due to increased competition.

I think the chances of Onyx fizzling are reasonably low, and the upside potential is very good. The price ($29.65 as I write) strikes me as still not taking into account its full future profit making potential if Carfilzomib is approved, but it isn't in the bargain basement the way it was earlier this year (52 week low $19.54).

See also:

Onyx Pharmaceuticals site

My Onyx Pharmaceuticals main page

Friday, November 19, 2010

HILL, DNDN, ONXX, SGI, MCHP, NVDA, AMAT

I have gotten terribly behind, this is hardly a log at all of late ...

Here are links to my summaries of recent Q3 analyst conference calls. Lots of interesting stuff, but I am unlikely to do separate commentary on all of them.

Dot Hill Q3 2010 Analyst Conference Call Summary. First quarter with non-GAAP profits in some time, appears to be on a good projectory with new storage products.

Dendreon Q3 2010 Analyst Conference Call Summary. About as expected, ramped up Provenge sales to the max until they get facility expansion permission.

Onyx Pharmaceuticals Q3 2010 Analyst Conference Call Summary. An exceptional quarter due to a large upfront payment from Japan.

SGI Q3 2010 Analyst Conference Call Summary. Still in the red, but new supercomputer sales are ramping rapidly.

Microchip Q3 2010 Analyst Conference Call Summary. Excellent revenues and profits.

NVIDIA Q3 2010 Analyst Conference Call Summary. Promises of Tegra revenues from future products.

Applied Materials Q3 2010 Analyst Conference Call Summary. Excellent quarter, demand for semiconductor manufacturing equipment remains strong, even the solar division was in the black.

Marvell is way up today after great results reported yesterday. If you think this was a good quarter, wait until revenues for chips for the new smartphones in China kick in next year. See Marvell Q3 2010 Analyst Call Summary.

Thursday, November 11, 2010

Cisco Leads Market Lower After Conference

The market is being led lower by Cisco (CSCO) today. Yesterday Cisco released slightly disappointing results and, at its analyst conference call, gave very disappointing guidance for the current quarter, which is Cisco's Q2 fiscal 2011.

In short, government spending is a big part of Cisco's pie, and government spending, especially by American states that have balanced-budget provisions, was weak. A second area of weakness was sales of set top boxes to cable companies.

For a more detailed report try my Cisco fiscal Q1 2011 analyst conference call summary.

I don't own Cisco stock.

Up today is NVIDIA. But I have other conferences to cover for clients, so I may not be posting my NVDA conference call summary (Q3 fiscal 2011) until late tonight or even Friday. But you can bookmark the page and return to it later.

For a complete list of technology stocks I cover for the public, see analyst conference call list.

In short, government spending is a big part of Cisco's pie, and government spending, especially by American states that have balanced-budget provisions, was weak. A second area of weakness was sales of set top boxes to cable companies.

For a more detailed report try my Cisco fiscal Q1 2011 analyst conference call summary.

I don't own Cisco stock.

Up today is NVIDIA. But I have other conferences to cover for clients, so I may not be posting my NVDA conference call summary (Q3 fiscal 2011) until late tonight or even Friday. But you can bookmark the page and return to it later.

For a complete list of technology stocks I cover for the public, see analyst conference call list.

Tuesday, November 9, 2010

AMD Ships First APUs on Analyst Day

Computer chip maker AMD announced it began shipping its new APUs (Advanced Processing Units) to computer makers this morning from its Singapore plant. At its analyst day presentation AMD executives described and demonstrated the APUs, which combine an advanced CPU (general purpose computer processing unit) with an advanced GPU (graphics processing unit) on a single chip.

Emphasizing what a groundbreaking point has been reached, CEO Dirk Meyer held up a typical sized CPU and then a mid-range GPU card, which was about the size of a small paperback book. Then he held up the APU that will have the equivalent CPU and GPU computing power. It was smaller than the CPU chip, about the size of a postage stamp. I know that the GPU card contains not only a GPU chip but memory, a fan, and connections for video output, so the comparison was a bit of an exageration. But it is a sort of computing grail achievement that goes beyond mere size comparisons.

Of course, knowing AMD has been working for years to achieve this feat, much larger rival Intel has announced that it will also have an integrated cpu/gpu product release for 2011. AMD executives mocked it, as well they might. We know it is an inferior product. It supports a graphics standard called DX10, which is now four years old. AMD supports DX11. It is true that most older software and games can't take advantage of DX11.

But many games already can, and most graphics software updates are moving to DX11. So Intel will be making an offering that can't cope with new games or software. When you buy a new computer, it is often because you want to take advantage of new software. Intel will be leaving consumers in the lurch.

Nevertheless, Intel is the Goliath, and AMD's previous attempts to take on the giant have had mixed results. Intel's profits are usually higher than AMD's revenues, and Intel spends way more on R&D than AMD. A few years ago Intel was so far behind in graphics, it is remarkable that they are maybe only 2 years behind now.

Intel will heavily outspend AMD in marketing, and will omit to tell consumers that its chips can't run DX11. So for AMD to take a lot of market share in 2011, it has to get its story out. In my experience retailers are more interested in Intel advertising subsidies than in making sure consumers make an informed choice between computers based on AMD and Intel. I would hope that tech "geniuses" would tell show off their stuff by telling the public to choose AMD if they want good graphics and video capabilities. But it seems that a lot of technology mavens are employed by Intel and Apple.

If the word does get out that Intel cpu/gpu combination chips are not good enough, AMD's ability to take market share could become capacity constrained. Intel has a huge production capability to match its market share; AMD's capacity can only be expanded so much in the short run.

Still, even a 10% increase in revenues for AMD in 2011, with maybe a 1% increase in market share, would be a boon for AMD.

Watch this space closely. The actual computers will start being available to the public in January, traditionally a slow period for computer sales. Public acceptance of the new AMD products, or resistance to Intel advertising, should be knowable by March or so, and act as a predictor for the remainder of the year.

For investors a key element will be margins. AMD believes that with the new processors (and server chips introduced in 2010) it can improve its non-GAAP gross margin from about 40% for 2010 to about 44% to 48% in 2011. If that turns out to be true (if Intel does not start a price war), then earnings will rise nicely and AMD will be in an even better position to compete with Intel in 2012.

Dirk Meyer showed an HP thin light notebook running gaming level graphics using the new APU chips. He claimed it could run 8 to 10 hours on one battery charge, and would cost less than $600. I want one, and it would work a lot better for me than a smaller form factor tablet computer. This ability to reduce power consumption is being introduced across the range of new AMD products in 2011: for netbooks, notebooks, desktops, and servers. That is good news.

Emphasizing what a groundbreaking point has been reached, CEO Dirk Meyer held up a typical sized CPU and then a mid-range GPU card, which was about the size of a small paperback book. Then he held up the APU that will have the equivalent CPU and GPU computing power. It was smaller than the CPU chip, about the size of a postage stamp. I know that the GPU card contains not only a GPU chip but memory, a fan, and connections for video output, so the comparison was a bit of an exageration. But it is a sort of computing grail achievement that goes beyond mere size comparisons.

Of course, knowing AMD has been working for years to achieve this feat, much larger rival Intel has announced that it will also have an integrated cpu/gpu product release for 2011. AMD executives mocked it, as well they might. We know it is an inferior product. It supports a graphics standard called DX10, which is now four years old. AMD supports DX11. It is true that most older software and games can't take advantage of DX11.

But many games already can, and most graphics software updates are moving to DX11. So Intel will be making an offering that can't cope with new games or software. When you buy a new computer, it is often because you want to take advantage of new software. Intel will be leaving consumers in the lurch.

Nevertheless, Intel is the Goliath, and AMD's previous attempts to take on the giant have had mixed results. Intel's profits are usually higher than AMD's revenues, and Intel spends way more on R&D than AMD. A few years ago Intel was so far behind in graphics, it is remarkable that they are maybe only 2 years behind now.

Intel will heavily outspend AMD in marketing, and will omit to tell consumers that its chips can't run DX11. So for AMD to take a lot of market share in 2011, it has to get its story out. In my experience retailers are more interested in Intel advertising subsidies than in making sure consumers make an informed choice between computers based on AMD and Intel. I would hope that tech "geniuses" would tell show off their stuff by telling the public to choose AMD if they want good graphics and video capabilities. But it seems that a lot of technology mavens are employed by Intel and Apple.

If the word does get out that Intel cpu/gpu combination chips are not good enough, AMD's ability to take market share could become capacity constrained. Intel has a huge production capability to match its market share; AMD's capacity can only be expanded so much in the short run.

Still, even a 10% increase in revenues for AMD in 2011, with maybe a 1% increase in market share, would be a boon for AMD.

Watch this space closely. The actual computers will start being available to the public in January, traditionally a slow period for computer sales. Public acceptance of the new AMD products, or resistance to Intel advertising, should be knowable by March or so, and act as a predictor for the remainder of the year.

For investors a key element will be margins. AMD believes that with the new processors (and server chips introduced in 2010) it can improve its non-GAAP gross margin from about 40% for 2010 to about 44% to 48% in 2011. If that turns out to be true (if Intel does not start a price war), then earnings will rise nicely and AMD will be in an even better position to compete with Intel in 2012.

Dirk Meyer showed an HP thin light notebook running gaming level graphics using the new APU chips. He claimed it could run 8 to 10 hours on one battery charge, and would cost less than $600. I want one, and it would work a lot better for me than a smaller form factor tablet computer. This ability to reduce power consumption is being introduced across the range of new AMD products in 2011: for netbooks, notebooks, desktops, and servers. That is good news.

Sunday, November 7, 2010

TTM Technologies Validates New Model

If you owned TTMI (TTM Technologies), America's largest manufacturer of printed circuit boards (PCBs), at the beginning of the week and held it until the market closed on Friday, you saw your shares go from $10.52 to $13.63, or up 29.6%, with most of the advance made on Friday.

Why the sudden excitement? On Thursday TTM announced third quarter (Q3) results and held its analyst conference call. Essentially TTM's acquisition of Meadville, a Hong Kong based PCB manufacturer with facilities in mainland China, turned out to be a smart move. This was the first full quarter after the Meadville acquisition, so you can begin to see why TTM has set itself on track to be a global powerhouse in the coming decade.

But why was the stock price low to begin with? It is not that TTM had been doing badly, though it had its setbacks during the late recession. The background is that the PCB industry in the U.S. has been shrinking for over a decade, even as global PCB demand rose. Manufacturing moved to other nations, most notably China. This was especially true for volume production, like consumer items that have runs of 100,000 units or more.

To keep itself profitable TTM, and some competitors like DDi (DDIC) has specialized in making boards in smaller batches, and in particular when newer technologies are required. Small batches can be prototypes for larger production runs, or can be for industrial or medical instruments where only a few, or a few hundred, boards are needed. TTM provides a level of expertise in designing and manufacturing boards for the new, micro-sized electronic components that few PCB companies in the world can match. They are able to charge for that expertise and maintain a good profit margin. Even in the first quarter of 2009, TTM squeezed out a profit on lower revenues.

Meadville does do large scale PCB manufacturing in China, but mostly at the high end, for instance for Apple products. So their profit margins were also good. For years TTM looked to acquire an Asian PCB manufacturing so they could help their customers on large production runs. In theory the new model is: prototype the PCB in American facilities of TTM, then do large runs in TTM's China facilities.

However, so far mostly we are just seeing that Meadville was a well-run, profitable business, that TTM paid a fair price for it, and that the resulting combination is about as profitable as it looked like it would be.

For Q3 2010, revenues were $357.8 million, up 15% sequentially from $310.2 million and up 157% from $139.1 million in the year-earlier quarter. GAAOP net income was $32.1 million, up by a factor of 4.8 sequentially from $6.7 million and up from negative $4.9 million year-earlier. Resulting in GAAP EPS (earnings per share) of $0.36, up 6x sequentially from $0.06 and up from negative $0.11 year-earlier.

If you use $0.35/share as the new run rate, TTM is generating $1.40 in earnings per year. So even at Friday's closing price the rate of return is very attractive.

One thing to watch, however, is debt. Meadville had acquired a lot of debt in expanding its facilities, and now TTM has taken on that debt. Interest rates are favorable and plenty of cash is being generated to pay off the debt over time, but it is still a negative.

For more detail you can read my Q3 2010 TTM Technologies (TTMI) analyst call summary

And of course the TTM web page.

Why the sudden excitement? On Thursday TTM announced third quarter (Q3) results and held its analyst conference call. Essentially TTM's acquisition of Meadville, a Hong Kong based PCB manufacturer with facilities in mainland China, turned out to be a smart move. This was the first full quarter after the Meadville acquisition, so you can begin to see why TTM has set itself on track to be a global powerhouse in the coming decade.

But why was the stock price low to begin with? It is not that TTM had been doing badly, though it had its setbacks during the late recession. The background is that the PCB industry in the U.S. has been shrinking for over a decade, even as global PCB demand rose. Manufacturing moved to other nations, most notably China. This was especially true for volume production, like consumer items that have runs of 100,000 units or more.

To keep itself profitable TTM, and some competitors like DDi (DDIC) has specialized in making boards in smaller batches, and in particular when newer technologies are required. Small batches can be prototypes for larger production runs, or can be for industrial or medical instruments where only a few, or a few hundred, boards are needed. TTM provides a level of expertise in designing and manufacturing boards for the new, micro-sized electronic components that few PCB companies in the world can match. They are able to charge for that expertise and maintain a good profit margin. Even in the first quarter of 2009, TTM squeezed out a profit on lower revenues.