AMD (Advanced Micro Devices) has only two competitors in its niche: Intel (INTC) for CPUs (computer processing chips) that run x86 software and NVIDIA (NVDA) for GPUs (graphics processing chips). How much market share it takes in the PC chip market, and what margins it receives on the chips it does sell, determines its levels of revenue and profit or loss.

Historically, while AMD has been innovative, it has come in a far second against Intel and NVIDIA. In the last two years it has lost ground to Intel and gained ground from NVIDIA. The picture has been complicated further by the emergence of ARM architecture based processors as the preferred basis for smaller mobile devices like smartphones and tablet computers.

After years of development (usually corresponding to quarterly earnings losses) this year AMD is selling chips that combine a CPU and a GPU. Intel, also, has appended graphics to its new line of CPUs, but their chips are remarkably inferior, incapable of running the current Windows graphics standard, DirectX 11. As a result AMD has been selling all the Fusion chips it has been able to make.

Why then, the lack of excitement and lack of upward momentum in AMD stock? Today AMD closed at $6.92, well off its 52-week high of $9.58 and with an astonishingly low P/E ratio of 6.4, the kind you would expect from a declining industry stock.

For the moment the most visible cutting edge technology is in smartphones and Apple and Android based small tablets. That pretty much sums up tech investor thinking about AMD: that a tidal wave of 7 inch screens are going to replace PCs, including both notebook computers and desktops that can run 60 inch displays.

Let's say you have discovered the limits of small screen computing and think there is still life left in the larger form factors. How should AMD be priced then?

First—even if the economy lags, even if consumers are careful with their holiday electronics purchases, even if the economies of India and China don't grow quite as fast in 2011 as they did in 2010—in Q3 and more so in Q4 AMD will get a significant boost in profits from its new Bulldozer CPUs for the server market. They began shipping in quantity earlier this month, with most of the early allotment going directly into the supercomputer market, where they will replace, or fill empty slots in, the prior generations of AMD Opteron processors. Profit margins are better for server chips than for PC chips. AMD has lost a lot of market share to Intel in server chips these last five years. The new chips should help regain market share. They have a different architecture than the Intel chips, and hence are very cost effective at certain workloads. Bulldozer is not a conquer-the-world chip, but it will keep AMD in the most profitable part of the server CPU game.

On the down side, there are so many rumors about yields (% of good processors on a die) being poor for the Fusion chips, that I think it is fair we can treat the rumors as true. At the next AMD analyst conference there should be a question about that. At the Q2 conference the closest answer we got was that margins were good on the Fusion chips. If both are true, and AMD was right about 2nd half margin improvements, then what we have is upside potential. Yields usually improve over time; if margins are already good, they should be great when yields improve. The problem was doubtless forging the CPU and GPU on the same die; traditionally these chip types used different silicon technologies. Bulldozer yields are rumored to be good, but then these server chips don't have a GPU component.

For now I would take Q3 guidance as a fair range. The economy might push revenues down, but yield improvements could push margins up. Guidance was for Q3 revenue to increase 8 to 12% sequentially. Note that because of holiday demand, Q3 is typically the strongest quarter for AMD.

The numbers, when reported, give us hard data, but the technology trends rule long-term value. I think AMD (and for that matter Intel) are over-discounted. I think both will be taking market share in the tablet market in 2012 and 2013. I think the PC market will stay healthier than most pundits predict. Consumers and businesses who skipped a desktop or notebook upgrade to buy a tablet and smartphone will get back on the upgrade cycle.

The combination of full-powered GPUs and CPUs on a single chip may be more revolutionary than the smartphone. Essentially, we are introducing desktop (or even notebook) parallel supercomputing. We are just beginning to see software applications that utilize either a CPU plus separate GPU or the new Fusion chips. So watch for companies like Microsoft, Adobe, and Autodesk, as well as lesser-known companies and startups, to take advantage of this new paradigm.

Disclosure: I am long AMD.

Showing posts with label AMD Fusion. Show all posts

Showing posts with label AMD Fusion. Show all posts

Monday, September 19, 2011

Sunday, July 24, 2011

AMD Key Question

AMD had a big jump in stock prices Friday, after reporting Q2 results after the market closed on Thursday. Q2 was not a stellar quarter, but AMD reported that its Fusion line of processors that combine a CPU and a GPU on single chip are ramping nicely. OEMs like them and consumers like them, so the demand is there. Intel, AMD's far larger rival, cannot match them. So it predicted a much better Q3.

If good time were more obviously ahead AMD's stock price would be far higher. Assuming AMD continues to release new Fusion projects, as well as its high-end CPU Bulldozer chips, on schedule, we still can't assume AMD will pick up appreciable market share from Intel.

Intel's law breaking, monopolistic practices days might be behind it, but it still has oodles of money it can throw at problems. It's problems are multiplying, to be sure, but it has a mountain of cash and a cascade of cash flow, unlike AMD.

An analyst at the Q&A part of the Thursday conference asked if Intel is going to lower its prices to compete with AMD Fusion. Let me quote my own summary of AMD's Q2 2011 conference, which is probably not an exact quote of the question and response:

Q. In the past when AMD has done well, we have seen price aggression from Intel. What are you seeing now?

A. It has always been a competitive market. The strength of our products will bring our plans to fruition.

In other words, not so much price aggression so far, but AMD is aware of the potential problem.

I believe Intel is somewhat constrained in its ability to lower prices. This is because investors are worried about Intel. Intel has about 80% of the market. To significantly lower prices on 80% of the market to keep AMD from gaining a percentage point here or there would cause Intel margins to drop, endangering the very cash flow that is such a competitive advantage. Also, the share AMD can take is limited by its production capabilities, which are very limited compared to Intel's.

Instead, Intel will rely on its marketing muscle. It will spend more on advertising, expecially the kind of "Intel inside" deals that convince retailers to promote computers with Intel CPU's instead of those with AMD Fusion chips. Intel will also keep trying to play catch up in the graphics arena. Intel is an entire generation behind AMD (and NVIDIA) in graphics technology, but they have been doing a good job in catching up, including by licensing technology from NVIDIA.

So again we have a situation where AMD has a window of opportunity, which should last until about the end of 2012. AMD will still be ahead in graphics and in integrating graphics with general cpu technology at the end of 2012, but going into the year 2013 Intel's combined GPU+CPU chips are likely to be good enough.

To really compound investor value AMD has to do great in 2012, generating enough money to keep up R&D and start exerting some advertising muscle of its own.

As far as the stock price goes, the Fusion chips are nice, but the real question is whether AMD will be able to pick up share in the server market with its upcoming Bulldozer based offerings. We won't begin to see if that is happening until we get results from Q4 2011 in January of 2012.

I own AMD stock, and I am cautiously optimistic, but I know how hard it is to compete with Intel's marketing machine, no matter how good AMD's chips may be.

See also amd.com

And my AMD summary page

Keep diversified!

If good time were more obviously ahead AMD's stock price would be far higher. Assuming AMD continues to release new Fusion projects, as well as its high-end CPU Bulldozer chips, on schedule, we still can't assume AMD will pick up appreciable market share from Intel.

Intel's law breaking, monopolistic practices days might be behind it, but it still has oodles of money it can throw at problems. It's problems are multiplying, to be sure, but it has a mountain of cash and a cascade of cash flow, unlike AMD.

An analyst at the Q&A part of the Thursday conference asked if Intel is going to lower its prices to compete with AMD Fusion. Let me quote my own summary of AMD's Q2 2011 conference, which is probably not an exact quote of the question and response:

Q. In the past when AMD has done well, we have seen price aggression from Intel. What are you seeing now?

A. It has always been a competitive market. The strength of our products will bring our plans to fruition.

In other words, not so much price aggression so far, but AMD is aware of the potential problem.

I believe Intel is somewhat constrained in its ability to lower prices. This is because investors are worried about Intel. Intel has about 80% of the market. To significantly lower prices on 80% of the market to keep AMD from gaining a percentage point here or there would cause Intel margins to drop, endangering the very cash flow that is such a competitive advantage. Also, the share AMD can take is limited by its production capabilities, which are very limited compared to Intel's.

Instead, Intel will rely on its marketing muscle. It will spend more on advertising, expecially the kind of "Intel inside" deals that convince retailers to promote computers with Intel CPU's instead of those with AMD Fusion chips. Intel will also keep trying to play catch up in the graphics arena. Intel is an entire generation behind AMD (and NVIDIA) in graphics technology, but they have been doing a good job in catching up, including by licensing technology from NVIDIA.

So again we have a situation where AMD has a window of opportunity, which should last until about the end of 2012. AMD will still be ahead in graphics and in integrating graphics with general cpu technology at the end of 2012, but going into the year 2013 Intel's combined GPU+CPU chips are likely to be good enough.

To really compound investor value AMD has to do great in 2012, generating enough money to keep up R&D and start exerting some advertising muscle of its own.

As far as the stock price goes, the Fusion chips are nice, but the real question is whether AMD will be able to pick up share in the server market with its upcoming Bulldozer based offerings. We won't begin to see if that is happening until we get results from Q4 2011 in January of 2012.

I own AMD stock, and I am cautiously optimistic, but I know how hard it is to compete with Intel's marketing machine, no matter how good AMD's chips may be.

See also amd.com

And my AMD summary page

Keep diversified!

Tuesday, November 23, 2010

AMD versus Intel: Show Me the DX 11

New computers in 2011 based on competing processors from Intel and AMD will initiate a new era in personal computing: the combination of a CPU and GPU (graphics processing unit) on a single chip. Intel's offering is refered to as Sandy Bridge; AMD's is Brazos (part of the Fusion program). In both cases a line of processors will be introduced that will be distinguished by part numbers. Systems are being built now and should be first available to consumers in January, with many more systems and variations on the processors available as 2011 progresses.

Over the last decade in particular graphics processing has increased in importance for the vast majority of computer users. People watch and even edit video on a regular basis. 3D virtual realities, including games, are a common part the computer experience. Even business applications are increasingly visual and three dimensiona. Starting with Windows Vista, computers needed improved graphic computation just to allow the operating system to present all of its graphic features.

If there is one thing consumers (including business buyers) need to know about computer graphics, it is that DX 11, introduced with Windows 7 in 2009, is the graphics standard for today's applications. DX 11 is short for DirectX 11, which Microsoft designed to handle multimedia, including video and 3D graphics. The prior generation, DirectX 10, was introduced in 2006. While a powerful advance in that era, it is now seriously out of date. While many applications still use DX 10, most new software introduced in 2011 will run best with DX 11. When DX 11 is not available, they will default to the lower graphics standards of DX 10 or earlier.

When a computer runs a DX 11 game or application by substituting DX 10, it loses graphic details that enhance the visual experience.

Sandy Bridge cannot run DX 11. If you buy a computer with an Intel Sandy Bridge processor, you will have two choices. Sub-optimal graphics, or buying an add-in graphics card from AMD or NVIDIA. AMD's Brazos chips (and all their Fusion chips to be introduced in 2011), on the other hand, do run DX 11. If you think about the computer replacement cycle, this is a remarkable difference. Intel computers bought in 2011 can be expected to remain in use for 2 to 4 years. By the end of that cycle they will be running a decade-old graphics standard.

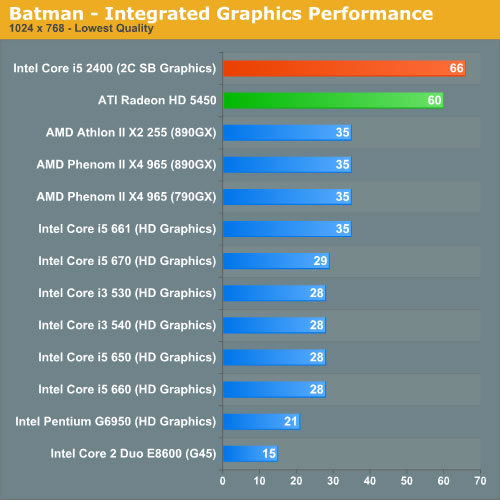

Intel is going to spend a hefty amount of money trying to convince people that Sandy Bridge based computers have graphics on par with AMD Brazos based computers. I've seen some of how that will work already. One online technology reviewer in England used a factually correct article that first appeared at Anandtech to argue that Sandy Bridge is about as good, possibly better, than AMD offerings. He used the following graphic to support his argument [see also the full Sandy Bridge Preview at Anandtech]:

What you see hear is that a desktop Sandy Bridge Core i5 (the top bar) shows a good improvement on Intel's earlier integrated graphics attempts. It is also significantly better, for this particular game, than a AMD Radeon 5450 card. That is great, but it is not a valid comparison for people buying new computers in 2010. The Radeon 5450 card, as you can see from the chart, could do remarkable things for an older Intel CPU with integrated graphics. But it is a card you can now get, retail, for $33.99 [See HD 5450 at TigerDirect]. It supports DX 11. It is the very bottom of the AMD discrete graphics line.

Fair enough, though, Sandy Bridge has the graphics equivalance of the cheapest, slowest discrete video cards made with AMD graphics chips, except it can't do DX 11. Brazos has, as its graphics engine, the equivalent of either a Radeon HD 6250 or 6310, depending on the exact chip used, but those don't correspond to any discrete chips released by AMD. However, graphics capabilities of the Brazos APU are only slightly less than for the 5450.

The Brazos chips, draws just 9 watts of power in the C versions with 6250s, or 18 watts in the E versions with 6310s. The Intel Core i5 2400 draws 95 watts (according to Anandtech). In fact [See Sandy Bridge Preview] they list no Sandy Bridge CPU that draws less than 65 watts.

In other words, in order to make Intel integrated graphics look better than AMD APU graphics, you need to take an expensive, power-sucking chip designed for desktop computers and compare it to a relatively inexpensive, power-sipping chip designed for netbooks and notebooks. And the Intel based desktop computer won't do DX 11.

The way it works out, AMD is releasing its Fusion (combined CPU/GPU) notebook & netbook chips in January. Intel is releasing its desktop chips with integrated graphics January. So direct mobile to mobile and desktop to desktop comparisons are not available yet.

AMD will be releasing more powerful Bulldozer chips designed for desktops later in 2011. They will support DX 11. Intel uses Atom for its netbooks; expect no DX 11 support there.

DX 11 adoption is well underway. Games tend to adopt a new graphics standard most quickly, but only when new games are introduced. See a list of games with DX 11 support. Note that Windows 7 itself supports DX 11. Expect new versions of most major application programs coming out in 2011 and 2012 to support DX 11.

What consumers need to know is that Intel based computers are essentially defective as they come off the assembly lines unless (1) you just do simple tasks like e-mail that are not graphics intensive or (2) they include a discrete graphics card from AMD or NVIDIA.

Who will tell them that? Not Intel. And Intel's advertising budget is such that you can expect a lot of obfuscation in media outlets, including technology magazines and web sites dependent on Intel for much of their advertising revenue. Intel also pays many large retail chains to promote its products over AMD products (by paying for ads).

If anyone is going to get the truth out, it is the millions of ordinary tech people who help everyone else with their buying decisions year-in and year-out. If they can get the typical buyer to ask the typical seller, "Does it do DX 11?" then AMD is going to pick up a lot of market share in 2011. On the other hand, if they stick to the "Intel is the premium brand," line, AMD will continue to have a hard time getting its message heard.

Over the last decade in particular graphics processing has increased in importance for the vast majority of computer users. People watch and even edit video on a regular basis. 3D virtual realities, including games, are a common part the computer experience. Even business applications are increasingly visual and three dimensiona. Starting with Windows Vista, computers needed improved graphic computation just to allow the operating system to present all of its graphic features.

If there is one thing consumers (including business buyers) need to know about computer graphics, it is that DX 11, introduced with Windows 7 in 2009, is the graphics standard for today's applications. DX 11 is short for DirectX 11, which Microsoft designed to handle multimedia, including video and 3D graphics. The prior generation, DirectX 10, was introduced in 2006. While a powerful advance in that era, it is now seriously out of date. While many applications still use DX 10, most new software introduced in 2011 will run best with DX 11. When DX 11 is not available, they will default to the lower graphics standards of DX 10 or earlier.

When a computer runs a DX 11 game or application by substituting DX 10, it loses graphic details that enhance the visual experience.

Sandy Bridge cannot run DX 11. If you buy a computer with an Intel Sandy Bridge processor, you will have two choices. Sub-optimal graphics, or buying an add-in graphics card from AMD or NVIDIA. AMD's Brazos chips (and all their Fusion chips to be introduced in 2011), on the other hand, do run DX 11. If you think about the computer replacement cycle, this is a remarkable difference. Intel computers bought in 2011 can be expected to remain in use for 2 to 4 years. By the end of that cycle they will be running a decade-old graphics standard.

Intel is going to spend a hefty amount of money trying to convince people that Sandy Bridge based computers have graphics on par with AMD Brazos based computers. I've seen some of how that will work already. One online technology reviewer in England used a factually correct article that first appeared at Anandtech to argue that Sandy Bridge is about as good, possibly better, than AMD offerings. He used the following graphic to support his argument [see also the full Sandy Bridge Preview at Anandtech]:

What you see hear is that a desktop Sandy Bridge Core i5 (the top bar) shows a good improvement on Intel's earlier integrated graphics attempts. It is also significantly better, for this particular game, than a AMD Radeon 5450 card. That is great, but it is not a valid comparison for people buying new computers in 2010. The Radeon 5450 card, as you can see from the chart, could do remarkable things for an older Intel CPU with integrated graphics. But it is a card you can now get, retail, for $33.99 [See HD 5450 at TigerDirect]. It supports DX 11. It is the very bottom of the AMD discrete graphics line.

Fair enough, though, Sandy Bridge has the graphics equivalance of the cheapest, slowest discrete video cards made with AMD graphics chips, except it can't do DX 11. Brazos has, as its graphics engine, the equivalent of either a Radeon HD 6250 or 6310, depending on the exact chip used, but those don't correspond to any discrete chips released by AMD. However, graphics capabilities of the Brazos APU are only slightly less than for the 5450.

The Brazos chips, draws just 9 watts of power in the C versions with 6250s, or 18 watts in the E versions with 6310s. The Intel Core i5 2400 draws 95 watts (according to Anandtech). In fact [See Sandy Bridge Preview] they list no Sandy Bridge CPU that draws less than 65 watts.

In other words, in order to make Intel integrated graphics look better than AMD APU graphics, you need to take an expensive, power-sucking chip designed for desktop computers and compare it to a relatively inexpensive, power-sipping chip designed for netbooks and notebooks. And the Intel based desktop computer won't do DX 11.

The way it works out, AMD is releasing its Fusion (combined CPU/GPU) notebook & netbook chips in January. Intel is releasing its desktop chips with integrated graphics January. So direct mobile to mobile and desktop to desktop comparisons are not available yet.

AMD will be releasing more powerful Bulldozer chips designed for desktops later in 2011. They will support DX 11. Intel uses Atom for its netbooks; expect no DX 11 support there.

DX 11 adoption is well underway. Games tend to adopt a new graphics standard most quickly, but only when new games are introduced. See a list of games with DX 11 support. Note that Windows 7 itself supports DX 11. Expect new versions of most major application programs coming out in 2011 and 2012 to support DX 11.

What consumers need to know is that Intel based computers are essentially defective as they come off the assembly lines unless (1) you just do simple tasks like e-mail that are not graphics intensive or (2) they include a discrete graphics card from AMD or NVIDIA.

Who will tell them that? Not Intel. And Intel's advertising budget is such that you can expect a lot of obfuscation in media outlets, including technology magazines and web sites dependent on Intel for much of their advertising revenue. Intel also pays many large retail chains to promote its products over AMD products (by paying for ads).

If anyone is going to get the truth out, it is the millions of ordinary tech people who help everyone else with their buying decisions year-in and year-out. If they can get the typical buyer to ask the typical seller, "Does it do DX 11?" then AMD is going to pick up a lot of market share in 2011. On the other hand, if they stick to the "Intel is the premium brand," line, AMD will continue to have a hard time getting its message heard.

Monday, September 27, 2010

AMD Lowers Guidance, But Stock Price Rises ... Why?

On September 23, 2010, AMD, a maker of CPUs for servers and personal computers, made a big downward correction in its guidance [See AMD Update Third Quarter Outlook]. Yet the stock shot up from a base of $6.40 the next day, and since has risen to $7.02 at the close today. In the past few years, AMD stock has not done well on good news, much less bad news. What is the difference now?

Some pundits think Oracle may buy AMD. That makes no sense to me. Oracle may be in the market for a chip stock, but the idea would be to improve their datacenter hardware offerings, which are now based largely on Sun's old proprietary processors. AMD would bring a lot of baggage with it. The only attractive things about AMD would be its engineering teams, which are first-class, and its low price. Its market capitalization was just $4.73 billion end of today, and its non-GAAP P/E is 4.56, about as low as you can get.

Buying AMD would put Oracle in the desktop and notebook chip business, which are low-margin businesses. Oracle hates low margin business. They shut down a good part of Sun when they acquired it because margins were not high enough to please them. What Oracle needs is a smaller chip company with skills storage and networking chips as well as data processing. Marvell would be a good acquisition, but I doubt very much Marvell Technology would allow itself to be acquired. An even smaller company would make more sense.

Back to AMD, it is most likely that the stock price bounce had to do with short covering. Lots of people like to short AMD, which is the perennial loser in its competition with Intel. Intel had lowered its third quarter guidance weeks ago. In general the PC industry was known to be having a relatively slow Q3. I think the problem for the shorts was that AMD's problems were already built into the stock price. In fact, the new guidance could have been a lot worse. Then there are the Fusion products that will begin shipping in Q4 and ramp in Q1 2011. No short wants to be around to see what happens then.

When AMD's price rose after the announcements, the shorts had nowhere to go. They had to cover their bad bets. Momentum players jumped in too, taking advantage of the distress of the shorts.

AMD's new guidance is revenue for Q3 "in the range of down one to four percent as compared to revenue of $1.65 billion for the quarter ended June 26, 2010." What investors should be looking for when AMD actually reports Q3 numbers on October 14 is margins. Did they at least get good prices for the CPUs and GPUs they sold? After that, look at guidance for the release of Fusion APUs. All evidence is that they will be widely and happily adopted by OEMs that want to offer consumers better graphics capabilities than Intel can provide.

See also: Can AMD Ignite Fusion? [June 7, 2010]

AMD Q3 guidance given at Q2 analyst conference [July 15, 2010]

Note: I currently own AMD and Marvell stock, but not Intel or Oracle.

Keep diversified!

Some pundits think Oracle may buy AMD. That makes no sense to me. Oracle may be in the market for a chip stock, but the idea would be to improve their datacenter hardware offerings, which are now based largely on Sun's old proprietary processors. AMD would bring a lot of baggage with it. The only attractive things about AMD would be its engineering teams, which are first-class, and its low price. Its market capitalization was just $4.73 billion end of today, and its non-GAAP P/E is 4.56, about as low as you can get.

Buying AMD would put Oracle in the desktop and notebook chip business, which are low-margin businesses. Oracle hates low margin business. They shut down a good part of Sun when they acquired it because margins were not high enough to please them. What Oracle needs is a smaller chip company with skills storage and networking chips as well as data processing. Marvell would be a good acquisition, but I doubt very much Marvell Technology would allow itself to be acquired. An even smaller company would make more sense.

Back to AMD, it is most likely that the stock price bounce had to do with short covering. Lots of people like to short AMD, which is the perennial loser in its competition with Intel. Intel had lowered its third quarter guidance weeks ago. In general the PC industry was known to be having a relatively slow Q3. I think the problem for the shorts was that AMD's problems were already built into the stock price. In fact, the new guidance could have been a lot worse. Then there are the Fusion products that will begin shipping in Q4 and ramp in Q1 2011. No short wants to be around to see what happens then.

When AMD's price rose after the announcements, the shorts had nowhere to go. They had to cover their bad bets. Momentum players jumped in too, taking advantage of the distress of the shorts.

AMD's new guidance is revenue for Q3 "in the range of down one to four percent as compared to revenue of $1.65 billion for the quarter ended June 26, 2010." What investors should be looking for when AMD actually reports Q3 numbers on October 14 is margins. Did they at least get good prices for the CPUs and GPUs they sold? After that, look at guidance for the release of Fusion APUs. All evidence is that they will be widely and happily adopted by OEMs that want to offer consumers better graphics capabilities than Intel can provide.

See also: Can AMD Ignite Fusion? [June 7, 2010]

AMD Q3 guidance given at Q2 analyst conference [July 15, 2010]

Note: I currently own AMD and Marvell stock, but not Intel or Oracle.

Keep diversified!

Subscribe to:

Posts (Atom)